3 Tradable Trends That Are Fundamentally Supported

marketlan/iStock via Getty Images

Momentum investing has been on full display lately, with the market piling into whatever has recently gone up. This is dangerous behavior that frequently ends in trend followers holding the bag as prices return toward fair values.

There is a safer way to participate in hot stocks, and that is to only embrace the momentum when it is fundamentally supported and reasonable in valuation. With that in mind, here are 3 market trends that have both fundamental and valuation support.

- Small-cap surge

- Domestic over international

- Value outperformance

Small-Cap Surge

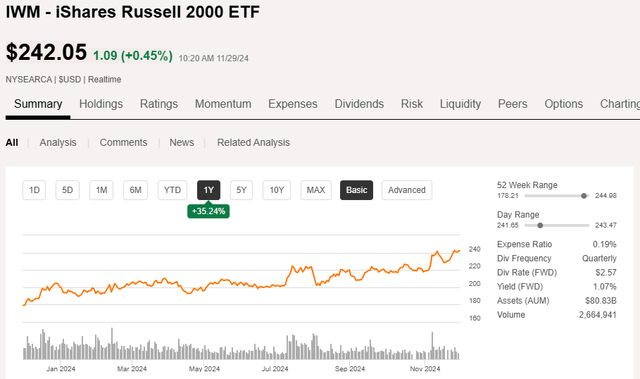

The iShares Russell 2000 Small Cap ETF (IWM) has significantly outperformed the S&P in the last month.

SA

This last month has added on to an already very strong year.

SA

While this sort of move would often push the investment into overvalued territory, small caps were generally cheap at the start of it having previously underperformed for years.

As such, valuation of small caps still looks reasonable relative to the rest of the market.

Additionally, there are two significant factors that fundamentally benefit small caps:

- Deregulation

- Reduced cost of capital

Large caps and mega caps benefit from more regulation because regulation tends to be a flat cost.

Depending on the industry, it might cost a publicly traded company something like $3-$5 million annually to comply with all the various regulations. This sum is almost meaningless to those with trillion dollar market caps, and only a tiny burden to companies above $50B in market cap.

For small caps, however, $3-$5 million annually is backbreaking. The extremely expensive regulatory cost is why so many small cap REITs list on the Canadian stock exchange, even if they have mostly or even entirely U.S. properties and management.

Regulations do have some purpose in protecting consumers and investors, so like most things, deregulation is a tradeoff, and I am not here to opine on whether the new administration’s planned deregulation is overall good or bad. My intent is to stay neutral on politics and just focus on the investment implications.

Deregulation is beneficial to small caps. If the regulatory burden to run a company is trimmed, this flat increase to net operating profits will have a disproportionate benefit to smaller companies. A million dollars of cost savings is huge for a $500 million market cap company, and irrelevant to megacaps.

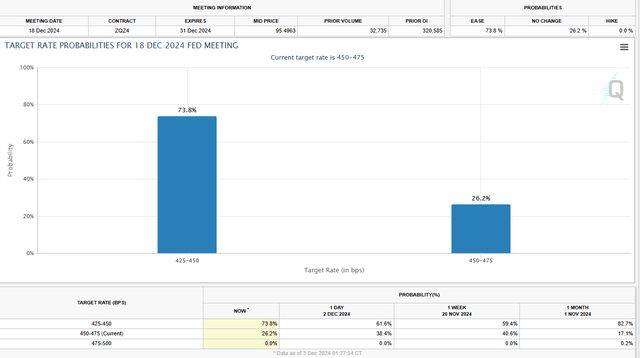

Small caps also stand to benefit disproportionately from reduced cost of capital from the Federal Reserve cuts. They have already cut 75 basis points, and it is currently considered a 73.8% chance (market implied odds) that they cut another 25 basis points in December.

CME Group

So far, the lower rates have not shown up in long-term treasuries, with the 10-year remaining stubbornly high at 4.215%.

However, the short end of the curve has dropped considerably, with SOFR dropping in parallel with the Fed Funds rate.

Small caps have significantly higher leverage than large caps, and they also use more variable rate debt. With much of this variable rate debt priced on SOFR, Fed cuts have directly reduced cost of capital for all companies, but disproportionately for small caps.

Domestic over international

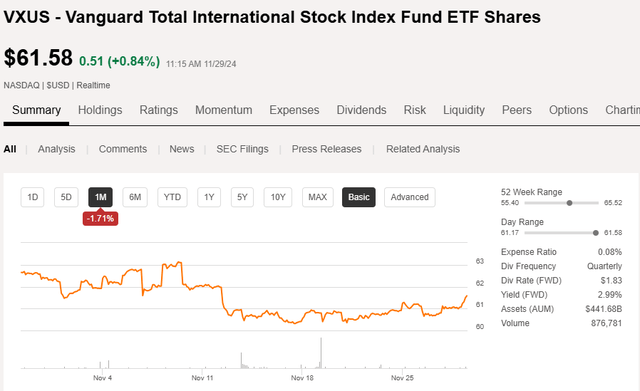

International stocks as measured by the Vanguard Total International Stock ETF (VXUS) have dropped in the last month even as U.S. stocks have broadly risen.

SA

This trend might continue, but I think a deeper layer has even better fundamental support.

Specifically, I believe companies that operate within a single country are better positioned than companies that operate across multiple countries.

In other words, a Chinese company operating in China could do well and a U.S. stock operating in the U.S. could do well, but Chinese companies relying on sales to the U.S. or U.S. companies relying on Chinese manufacturing could be in a tough spot.

President-elect Trump was hawkish on trade in his first presidency and is proposing even larger tariffs this time. Tariffs, like deregulation, are a tradeoff on which I will not opine on its overall value, opting instead to focus on the investment implications.

To the extent these tariffs are enacted, companies relying on international cross-border sales are likely to have reduced profitability, as tariffs will detract from the magnitude of surplus that is split between consumers and producers. On the positive side, companies with domestic supply chains are likely to have increased profitability, as the imported goods with which they currently have to compete will be less viable.

Value outperformance

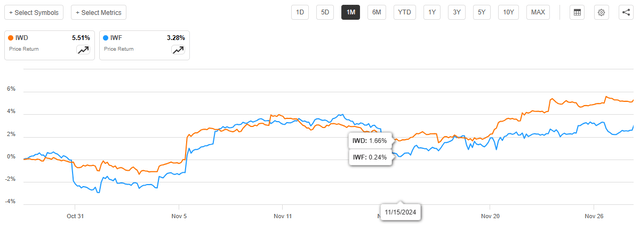

For the first time in a while, value has been outperforming as measured by the iShares Russell 1000 Value ETF (IWD) against the iShares Russell 1000 Growth ETF (IWF).

SA

This is in sharp contrast to the past few years, in which growth has outperformed value. That medium term underperformance sets value up nicely for some mean reversion. Value is cheaper relative to growth than normal, which would imply there is upside to value in the process of normalization.

I posit that one of the main reasons value has done poorly in the last few years is the aggressive antitrust environment.

Value is usually a key driver of M&A. When a company gets cheap enough, it becomes a highly accretive target for one of their peers. In the process of getting acquired, the purchase price is usually 10%-30% above market price, which results in the value company getting a nice bump in returns.

This value driven M&A has largely been shut down in the last few years, with the current FTC being extremely hawkish on mergers, particularly those in the same industry.

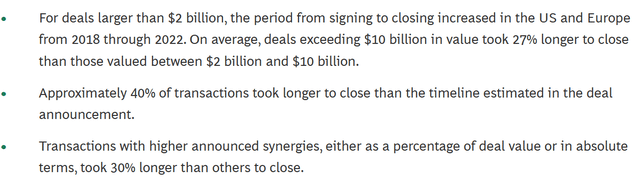

Boston Consulting Group reports that deals are taking longer to close, particularly those in the same industry with more synergy:

BCG

Many deals are also being blocked by FTC-driven lawsuits. Beyond the deals that are actually blocked, it serves as a deterrent to anyone who would even consider M&A.

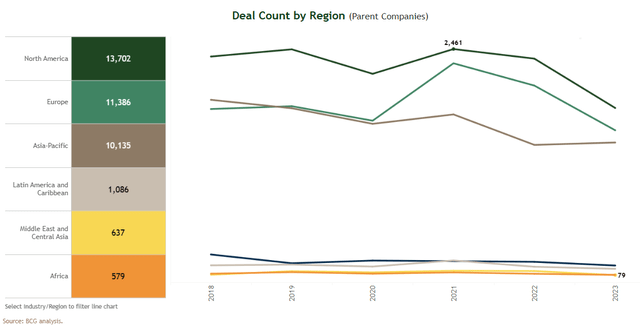

Lina Khan was sworn in as FTC chair in June 2021 and since then, deal volume has dropped materially in North America.

BCG

Andrew Ferguson has been announced as the new FTC chair and will likely be put in place in January.

Assuming antitrust goes back to a more historically normal environment, it should re-open the doors to companies buying their discounted peers.

This would bode well for value stocks trading at 50%-80% of peer earnings multiples, as these are the companies that are most likely to get return bumps from being acquired in M&A.

A return to a Fama French market

The famous Fama French 3-Factor Model described market performance as related to market risk, small-cap outperformance and value outperformance. That model has proven quite accurate over long periods of time but has failed to match the market in the last few years. The momentum heavy market caused megacaps and overvalued stocks to outperform, which is historically unusual.

Fundamental factors discussed above and price movements of the past few weeks suggest that we might be returning to a Fama French world.

Position accordingly.

link